Silicon-Based Scalability: The Strategic Shift in Quantum Investment

Quantum Motion has secured a €160 million Series C funding round, signaling a critical transition in the European quantum ecosystem. Co-led by DCVC and Mundi Ventures—through its deeptech vehicle Kembara—this capital injection underscores a growing investor preference for hardware that promises manufacturability over abstract performance metrics. With participation from the British Business Bank, Firgun Ventures, and heavyweights like Bosch and Porsche, the round places Quantum Motion firmly among Europe’s best-capitalized quantum entities, alongside peers like IQM and Pasqal.

This latest financial milestone arrives amid a surge in European quantum funding, which has reached €1.6 billion in 2025—a drastic acceleration from the €700 million recorded in the previous year. This volatility in capital distribution suggests that while quantum remains a high-risk venture, institutional investors have moved past the initial hype cycle, prioritizing firms with clear roadmaps to industrial production.

The Silicon Advantage: Leveraging CMOS Architecture

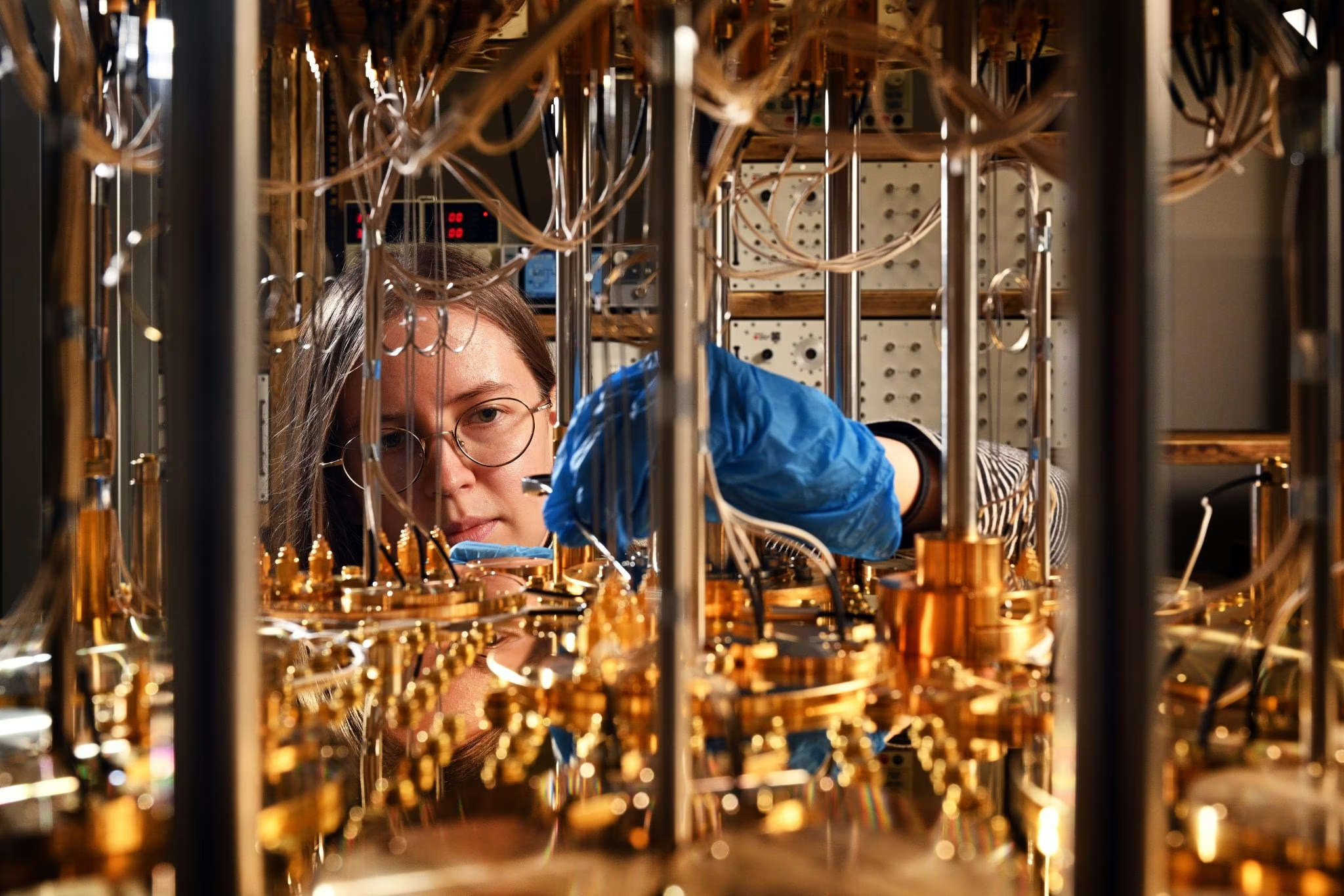

At the core of Quantum Motion’s investment thesis is its unique approach to qubit architecture. While many competitors oscillate between superconducting loops or trapped-ion systems that often require bespoke, exotic environments, Quantum Motion focuses on dot spin qubits. By storing quantum information in the spin of individual electrons trapped within silicon, the company aligns itself with the global semiconductor industry’s existing infrastructure.

The strategic importance of this choice cannot be overstated. By utilizing standard CMOS (Complementary Metal-Oxide-Semiconductor) manufacturing processes—facilitated by their partnership with GlobalFoundries—Quantum Motion is betting that the path to a fault-tolerant quantum computer is paved by scaling classical chip manufacturing. For industries wary of the massive infrastructure costs associated with non-silicon qubits, this approach offers a more pragmatic, cost-effective, and scalable supply chain.

Implications for the Post-Research Scalability Era

For the wider industry, Quantum Motion’s progress serves as a litmus test for the viability of silicon-based quantum processors. The company has already successfully delivered a quantum computer to the UK National Quantum Computing Centre (NQCC) that was built using industrial-grade semiconductor fabrication.

This is no longer a theoretical pursuit limited to university labs; it is a shift toward a manufacturing-centric methodology. By expanding its footprint into San Sebastian to collaborate with CIC Nanogune, the firm is further diversifying its talent pool and research capabilities, signaling that it is moving from the R&D stage toward formal commercialization.

Market Consolidation and the Qubit Race

The recent influx of megarounds in the European sector—including Quantum Motion, Pasqal, and Quanttware—indicates that the market is beginning to consolidate around companies that can demonstrate reproducible hardware results. As the industry matures, capital is flowing away from generalists and toward firms with tangible, scalable physical assets.

The quantum race is effectively entering its industrial revolution phase. For the pharmaceutical, AI, and financial sectors—all of which stand to be disrupted by quantum supremacy—Quantum Motion’s ability to leverage standard silicon fabrication may prove to be the deciding factor that differentiates lab-scale prototypes from commercially viable, mass-produced quantum infrastructure. This funding provides the runway necessary to prove that silicon spin qubits are not merely a curiosity of physics, but the backbone of the next generation of computing.