The Strategic Evolution of Experian: Scaling AI in a Regulated Landscape

Experian plc is aggressively transitioning from a traditional credit reporting bureau into a multifaceted, technology-first financial services powerhouse. The launch of the latest version of the Experian Virtual Assistant (EVA) serves as the architectural centerpiece of this strategy. By embedding generative AI into the consumer experience, Experian is attempting to bridge the gap between static credit data and dynamic, actionable financial management.

However, this transition is not merely a technical upgrade; it is a calculated effort to remain relevant in a market where personalized, AI-driven financial insights have become table stakes.

From Rules-Based Utility to Generative Intelligence

For years, Experian relied on a standard, rules-based chatbot to provide rudimentary credit advice. As consumer expectations for real-time interaction soared, these legacy systems became a bottleneck. The pivot to generative AI, initiated in late 2022, allowed the company to move beyond deterministic responses.

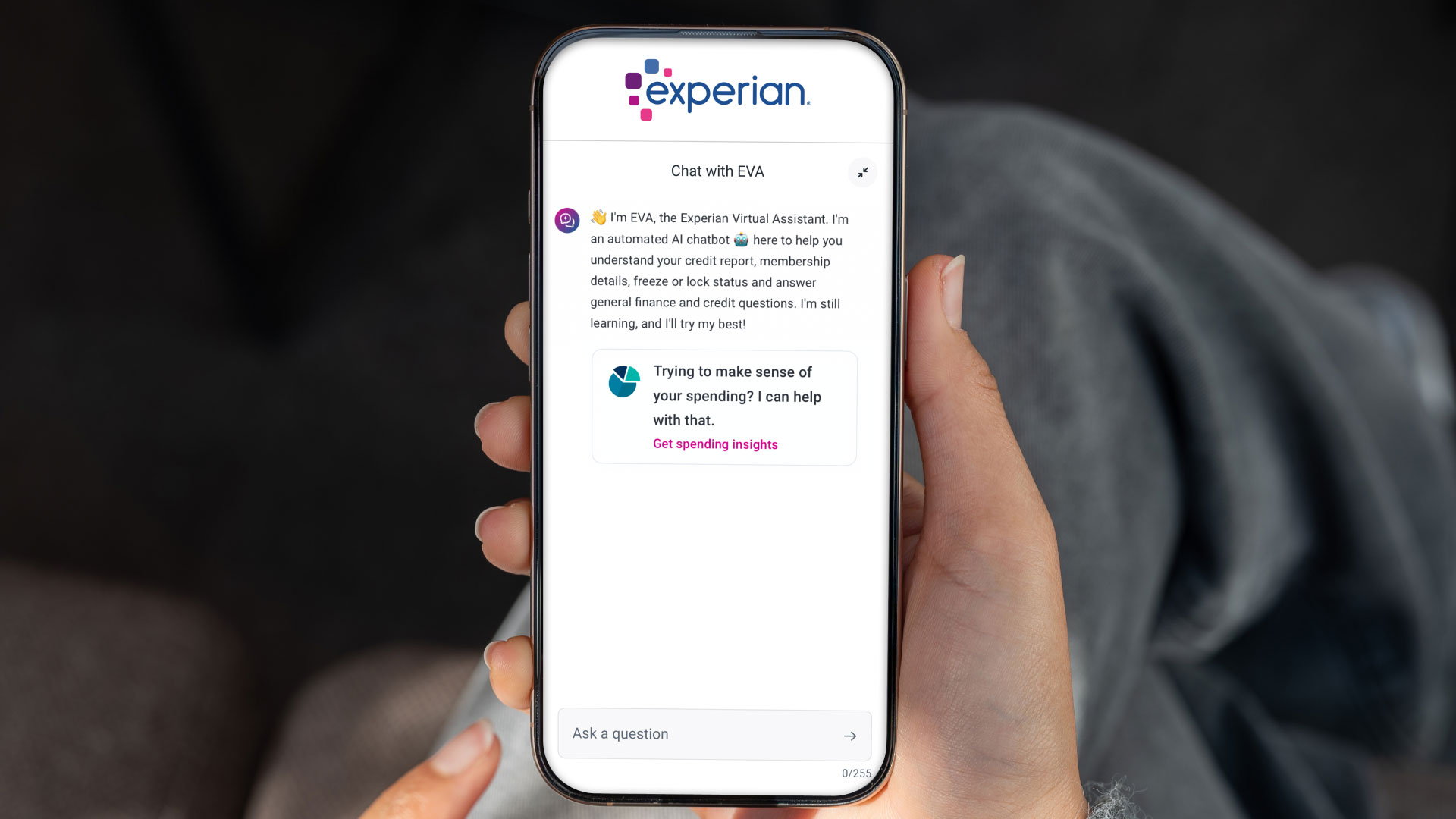

Version 3.0 of EVA represents a shift toward financial agency. By integrating open banking capabilities and connected accounts, the assistant now moves beyond explaining a credit score. It performs real-time diagnostics on consumer spending habits, identifying bloated recurring subscriptions and suggesting specific financial maneuvers—like initiating a credit freeze—directly through the interface. This shift toward task execution signals that Experian is positioning itself as a proactive financial concierge rather than a passive data repository.

Navigating the Regulatory Tightrope

The most significant barrier to scaling AI in the credit reporting sector is not capability, but compliance. Unlike consumer tech giants that prioritize rapid deployment cycles, Experian must operate under rigorous scrutiny.

Jack Yu, director of product management for generative AI, notes that the company subjects AI outputs to the same stringency as credit reporting data. This has led to a bifurcated approach to AI deployment:

- Governance-First Architecture: The system is engineered to distinguish between unauthorized advice—a licensed, regulated activity—and compliant financial guidance.

- Data Siloing: To mitigate privacy risks, sensitive consumer data is kept entirely separate from the generative models. Interactions are routed through secure, internal channels, ensuring that Large Language Models (LLMs) never store or learn from private financial records.

This internal friction—where compliance verification often outlasted the actual development hours—highlights the reality of AI adoption in the financial sector. Organizations must choose between rapid iteration and defensible compliance; Experian has chosen the latter, betting that its reputation for data integrity is its most valuable asset in an AI-saturated market.

Operational Efficiency and Edge Performance

Beyond regulatory hurdles, the development team faced intense technical pressure regarding latency. In the modern fintech ecosystem, a delay of even a few seconds can lead to user churn. To solve this, Experian optimized its infrastructure for real-time response streaming and sophisticated system routing.

This infrastructure work is part of a broader, decade-long investment in machine learning. While many competitors are sprinting to integrate LLMs to remain relevant, Experian’s backend has utilized behavioral analysis and fraud-detection models for years. The current iteration of EVA is simply the consumer-facing manifestation of these mature engineering capabilities.

The Competitive Implication

The financial application landscape is notoriously crowded. To survive, companies can no longer rely on simple data dashboards. The new EVA is designed to serve as a hub for Experian’s broader ecosystem, including its insurance marketplace and credit application services.

By positioning itself as an intelligent intermediary, Experian is creating a sticky user experience that keeps consumers within its orbit for diverse financial tasks. As Debbie Hsu, EVP of product at Experian Consumer Services, suggests, the goal is to transform the user journey from a transactional check on a credit score to a holistic, high-frequency financial engagement.

Ultimately, Experian’s success will hinge on whether it can scale these personalized experiences without eroding the foundational trust consumers place in the brand. For a data-centric institution, the AI age is not about replacing the advisor; it is about providing the tools that make the consumer their own most informed advocate.