Infrastructure Decoupling: The Strategic Intent Behind Google and Blackstone’s $25B AI Venture

Google and Blackstone have formalized a $25 billion joint venture aimed at institutionalizing compute-as-a-service. By combining massive capital deployment with proprietary silicon, the partnership signals a major shift in how AI training and inference resources are distributed, moving away from relying solely on public cloud provider multi-tenancy toward dedicated, high-performance infrastructure footprints.

The venture, which includes $5 billion in equity from Blackstone and additional debt financing, positions the firm as a primary provider of Google’s specialized hardware. Significantly, the initiative will be led by Benjamin Treynor Sloss, a key architect of Google’s cloud network and data center strategy, suggesting that this new entity is intended to mirror the operational efficiency of Google’s internal production environments on a commercial scale.

Breaking the GPU Monopoly with Vertical Integration

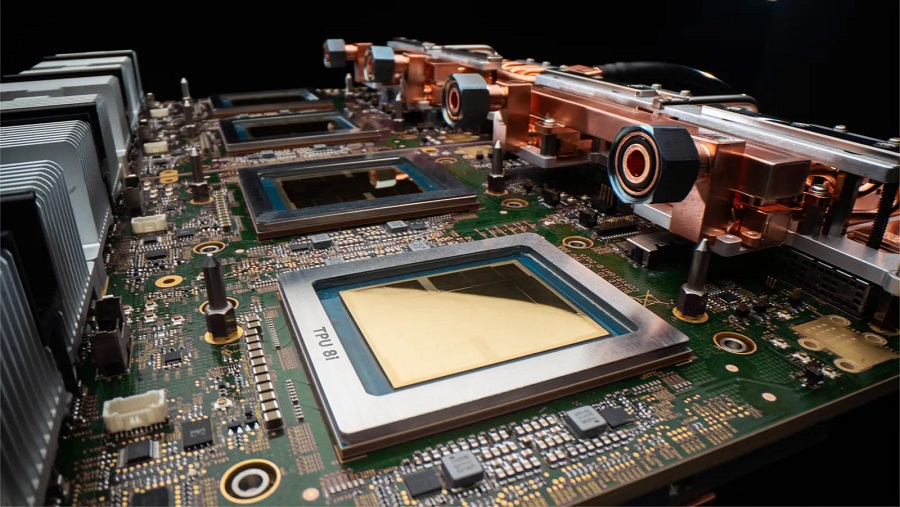

The core value proposition of this collaboration is the democratization of Google’s custom Tensor Processing Units (TPUs). By funneling these chips into a venture primarily owned by Blackstone, Google is creating an externalized ecosystem for its hardware. This is a direct competitive play against NVIDIA-heavy data centers.

The deployment of the new TPU 8t (training) and TPU 8i (inference) chips is central to this strategy. By integrating features like the SparseCore for enhanced data retrieval and the CAE engine for low-latency inference, these chips offer distinct performance advantages over general-purpose graphic processing units. Furthermore, the use of proprietary networking technology, such as TPUDirect, allows data packets to bypass traditional bottlenecks like CPUs, creating a tightly coupled, high-speed architecture that is notoriously difficult for standard enterprise environments to replicate.

Strategic Implications for Institutional Real Estate

For Blackstone, this move is a logical extension of its massive investment in digital real estate. With over $150 billion in existing data center assets—bolstered by acquisitions like QTS Realty Trust and Air Trunk—the firm is transitioning from a passive landlord to an active infrastructure operator.

By housing Google’s AI clusters within its vast property portfolio, Blackstone effectively creates a closed loop where energy, real estate, and high-performance computing combine to serve the growing needs of AI-native organizations. This 500-megawatt initial rollout is likely a baseline; as AI workloads demand increasing energy densities, Blackstone’s ability to leverage its massive footprint to secure power and space gives the joint venture a significant moat.

Industry Consequences: A Shift Toward Specialized Clusters

The broader market impact of this partnership cannot be overstated. We are witnessing the end of the generic cloud era. As AI models scale, companies are increasingly dissatisfied with the variable latency and performance inconsistency of traditional cloud instances.

By allowing these chips to be deployed directly into Blackstone-managed data centers, Google is facilitating a Cloud-in-a-Box model that provides the performance of an on-premise supercomputer with the management convenience of a capital-backed vendor. This will likely pressure other hyperscalers to reconsider their hardware exclusivity. As Blackstone evaluates its broader portfolio, we should expect to see these specialized computing nodes pop up globally, catering to financial services, pharmaceutical research, and large-scale synthetic data training—industries where latency and hardware efficiency are the primary drivers of competitive advantage.